Running the numbers

It is the biggest financial decision for many younger adults: Should I rent a home or buy one? The decision is especially difficult these days, with both interest rates and rents having risen in the past few years.

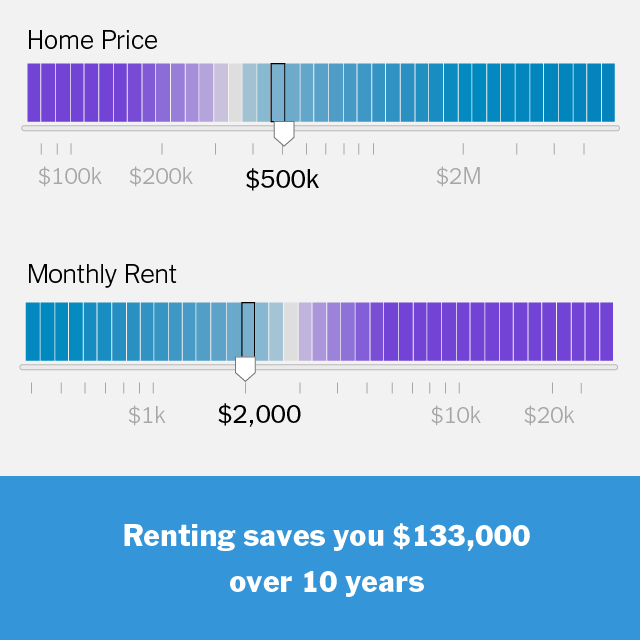

To help people understand the trade-offs, The Times has just relaunched its popular rent-versus-buy calculator. Even if you already own your home — or are a committed renter — you may enjoy playing with the calculator and learning a few things about the real estate market. I did.

The calculator, which The Times’s Upshot section built, has been updated in several important ways, including to take into account the 2017 tax law that affected the mortgage-interest deduction.

Ultimately, the calculator can’t tell you whether you should rent or buy. That decision depends on the future paths of home prices and rents, which are unknowable. It also depends on your life stage — a factor that too many people fail to consider when making this decision. If you know you will move again a few years from now, for instance, buying is almost certainly a mistake.

Here are a few other points that the calculator helps highlight:

It’s OK to rent

I know that many people feel guilty about renting — as if it’s an inherently inferior decision that wastes money. That’s wrong (as I explained on a recent “Daily” episode). When house prices are high, as they are in most parts of the U.S., buying often wastes more money because of broker’s fees, mortgage interest, house repairs and other costs of owning.

“At this time, in the majority of circumstances, renting likely makes more economic sense than buying,” said Mark Zandi, the chief economist at Moody’s Analytics, who has advised our work on the calculator over the years. He notes that the typical monthly mortgage is about $2,000 today, more than double what it was when the pandemic hit in early 2020.

Rents have risen, too, but not nearly as much. And many new rental units are coming on the market, which should hold down rents in the near future. The new units include higher-end, multifamily developments, like a 15-story, 1,111-unit complex on South Broad Street in Philadelphia.

An overrated deduction

The 2017 tax law reduced the advantages of owning a home in a way that many people have not fully recognized, said my colleague Francesca Paris, who helped build the new calculator. Francesca, who’s a renter, told me that she herself didn’t understand this dynamic until she worked on the calculator.

First, a bit of background: Taxpayers must choose between taking one large deduction, known as the standard deduction, and a series of individual deductions, known as itemized deductions, like the one for mortgage interest. If the standard deduction is more valuable to you, the itemized deductions become irrelevant.

The 2017 tax law, which was Donald Trump’s main domestic legislation, was mostly a tax cut, and it increased the value of the standard deduction. But the law also effectively reduced the value of itemized deductions in states with high taxes, like California, Illinois and New York. (Doing so created an incentive for states to cut their own taxes, a longtime goal of conservatives.)

This combination means that many homeowners now save more money by taking the standard deduction rather than itemized deductions. For them, the mortgage-interest deduction has become irrelevant.

The break-even rate

The calculator allows you to see the break-even mortgage rate that would make buying or renting more affordable (if the economy followed an expected path). In many situations, that break-even rate is between 4 percent and 5 percent, Francesca noted.

The average rate on a 30-year fixed mortgage is 7 percent today, up from less than 3 percent in early 2021 — which is a big reason that renting is often the smarter choice now.

When to buy

Buying will still make sense for some families. Home prices in large parts of the country — including New Orleans, Pittsburgh, St. Louis, upstate New York — are more reasonable. And even in expensive markets, families that are confident that they are going to remain in the same home for a decade or longer may prefer to own even if doing so costs extra.

For people tempted to buy, Zandi encourages looking at new construction. Prices of older homes haven’t fallen much as mortgage rates have risen, because owners can simply decide not to sell if they don’t get an offer they like. Developers are more likely to cut a deal. They lose money when homes sit empty, and many have cut the price of newly built homes, as the financial writer Wolf Richter has noted.

Use the calculator to explore these dynamics. As the housing market changes, you can check back to see how your calculations change.